Introduction: After the trough period in 2020, the rise of polyester filament has continued since 2021. The main driving force comes from the cost side. However, the raw materials still have upward momentum, and the rise of polyester filament may continue until early March.

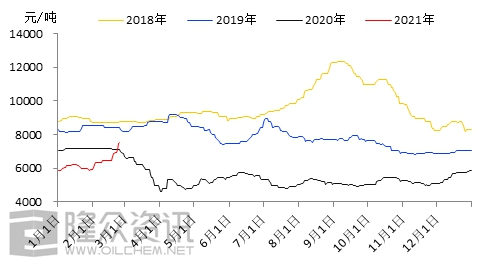

Figure 1 Price trend comparison of mainstream polyester filament models from 2018 to 2021:

Source: Longzhong Information

In recent years, since the large-scale refining and chemical project was put into operation, polyester filament has shown a volatile downward trend following the trend of PTA. Especially in 2020, the sudden epidemic has caused the entire chemical fiber industry to As the main textile and clothing fabric, polyester filament has not been spared. After experiencing a trough in the first half of 2020, polyester filament has gradually embarked on a rebound. Especially from the end of 2020 to the present, polyester filament yarn has enjoyed great growth relying on cost support.

Figure 2 Comparison of mainstream polyester filament models and raw material price trends:

Source: Longzhong Information

In the near future, oil prices continue to rebound during the Spring Festival holiday, vaccines are making good progress, the global trade environment has improved during the term of the new U.S. government, and the cold wave weather in the United States has also caused many sets of B2 The shutdown of alcohol equipment has triggered supply concerns, and ethylene glycol futures have frequently reached daily limit levels after the holiday. PTA Yisheng’s Hainan unit was unexpectedly shut down during the holidays, and the overall supply was lower than market expectations. The increase in oil prices boosted market sentiment. The short-term support period is now in the market. After the holiday, dual raw materials showed a sharp increase. Under cost pressure, polyester filament yarn Enterprise quotations have been raised one after another, and the market has been raised by a total of 600-700 yuan/ton. As of now, the reference price for POY150D/48F in Jiangsu and Zhejiang regions is 7450-7650 yuan/ton, the reference price for FDY150D/96F is 7550-7675 yuan/ton, and the reference price for DTY150D/48F is 8950-9100 yuan/ton.

According to statistics before the Longzhong Festival, downstream weaving companies resume work later than polyester production companies. However, due to the government’s promotion of celebrating the New Year in situ this year, about 30% of migrant workers Workers chose to stay in the local area for the holidays, and the price of polyester filament continued to rise. In addition, the epidemic was well controlled during the Spring Festival, and low-risk areas did not need to be quarantined after the holiday. Many factors ensured the orderly resumption of work after the holiday, and made the resumption of work earlier than scheduled. As of February 24, the comprehensive operating rate of chemical fiber weaving in Jiangsu and Zhejiang has increased to 44.50%. It is expected that the weaving operating load will increase to 80-90% by the end of February, and the weaving industry will basically resume normal operation in early March.

However, due to the rapid growth of polyester and raw materials at this stage, the excessive growth has aggravated market risks. Downstream mentality is cautious, end users are hesitant to “place orders”, and weaving companies place orders after the holiday. No significant improvement has been seen yet.

Based on the current situation, the cost-side support can last until around mid-March. Can this round of price increases be transmitted downward to the terminal, and whether the increase will affect polyester filament 3 The key to monthly market trends. Before the holiday, gray fabrics were sold at a loss, and the overall inventory pressure was not great. Recently, gray fabrics have followed the rise of polyester, and their quotations have been raised one after another. It is said that some traders are also collecting large quantities of fabrics. After the holiday, gray fabric inventories also show a downward trend.

Therefore, we expect that before mid-March, polyester filament yarns will continue to fluctuate and warm, and there is still some room for upward growth in transactions. During this period, due to fluctuations in raw materials, there will be a certain degree of adjustment, but there is no adjustment for the time being. Downgrade risk. However, after mid-March, terminal demand gradually became clear, and the excessive rise suppressed terminal demand to a certain extent. Therefore, market negotiations became stagnant after mid-March, and there was a risk of decline. </p