Weekly Industry Chain Operation Overview (02.20-02.27)

Views in this issue

(1) The impact of overseas epidemics continues to escalate, the situation in many countries has worsened, and energy demand has declined. Stirring concerns, international oil prices fell sharply, and the market focused on whether OPEC will deepen the production reduction agreement.

(2) Affected by the drop in oil prices this week, polyester raw materials returned to a downward trend. The current main problem is insufficient follow-up of downstream demand. Limited by the upgrade of protective measures against the epidemic by local governments, as well as traffic control and isolation periods for non-local workers returning to work, the progress of terminal resumption is limited. It is expected that polyester raw materials will still fluctuate weakly in the short term. Focus on the impact of the recent macro situation on market conditions.

(3) The polyester yarn market was overall weak this week, with transactions being deserted and only maintaining an average level of about 20%. As of February 27, the inventory days of polyester factories were approximately 26 to 37 days, and polyester yarn inventory has been greatly accumulated since the Spring Festival. At present, the recovery rate of terminal texturing and weaving operations is limited. It is expected that polyester yarn prices may fall in the short term, and inventory pressure will force manufacturers to cut prices and promote sales. Focus on macroeconomics, changes in terminal demand, crude oil and PTA trends.

Polyester factory polyester yarn operation overview

The overall production and sales of the polyester yarn market this week are light. Affected by the epidemic, the terminal resumption of work is still in progress, and the overall startup is Rates are limited. Since the Spring Festival holiday, polyester manufacturers have greatly accumulated inventory. As of February 27, it is estimated that polyester factories in Jiangsu and Zhejiang will have 26 to 37 days of inventory. It is expected that polyester prices will continue to fall in the short term.

In terms of production efficiency, compared with the decline in cost-end polyester raw materials, the price reduction of polyester yarn is smaller, and the overall profit margin is acceptable.

Semi-glossy slice price trend

The transaction price of semi-gloss slices fell by about 2.54% this week. Slice theory cash flow earnings were basically the same as last week. The short-term slice price shock is expected to be weak. In the later period, we will focus on the trend of polyester raw materials, device dynamics and changes in downstream demand.

Transaction status of China Textile City

The transaction volume of China Textile City from 02/21 to 02/27 totaled 7.59 million meters, of which 4.67 million meters were traded in chemical fiber cloths.

International crude oil weekly analysis

International oil prices have fallen sharply this week, with US oil and Brent oil both falling by more than 12%. As the global epidemic situation continues to escalate, the market is worried about future energy demand. At the same time, the recent plunge in U.S. stocks has intensified the risk of volatility in the global capital market. Although OPEC+ has proposed deepening production cuts to cope with the sharp drop in demand caused by the coronavirus, Russia’s attitude is currently ambiguous. Oil prices are expected to remain weak in the short term. Focus on the international economic situation and geopolitical influences.

U.S. EIA crude oil inventories for the week

Fundamental positive factors:

1. The U.S. Energy Information Administration (EIA) released a report on Wednesday (February 26) showing that as of February 21 That week, U.S. crude oil inventories increased by 452,000 barrels to 443.3 million barrels, while market estimates were for an increase of 2.467 million barrels. In addition, U.S. domestic crude oil production continued to remain flat at 13 million barrels per day last week.

2. The United States has imposed sanctions on a broker owned by Russian crude oil giant Rosneft, which may affect the crude oil exports of Venezuela, a member of the Organization of the Petroleum Exporting Countries (OPEC), combined with the sharp decline in Libyan crude oil production. , supply problems in the crude oil market began to emerge.

3. Affected by the continued blockade of crude oil export terminals, which has led to the suspension of production in several oil fields, the Libyan National Oil Company released data showing that as of February 25, Libyan crude oil production was approximately 136,000 barrels per day, which has dropped by more than one million barrels from the previous approximately 1.3 million barrels per day.

Fundamental negative factors:

1. The latest concern is that the number of new cases overseas has exceeded that in China. Yesterday, US President Trump held a media conference and emphasized that the epidemic in the United States is under control. Trump said the risk to Americans from the new coronavirus remains very low and he is ready to adjust and take all necessary measures as the epidemic spreads. He added, “We are ready…We have measures in place so that when the disease spreads, we are ready to do whatever we have to do, if it spreads. “But the market is not optimistic about this. At the same time, the new crown epidemic in South Korea has further worsened. South Korea’s Central Anti-epidemic Countermeasures Headquarters reported on the 27th that compared with 4 pm the previous day, South Korea had 505 more cases in one day. This means that South Korea’s 24-hour The number of confirmed cases exceeded that of China (433 cases) for the first time.

2. The Russian Energy Minister told reporters in Moscow on Thursday that the outbreak of the coronavirus outside China will lead to further reductions in oil consumption. According to the TASS news agency, Novak has previously mentioned relevant analysts’ expectations that the outbreak will reduce oil demand in 2020 by 150,000 barrels/day to 200,000 barrels/day. Although Russia admits that the impact of the epidemic on oil demand may will be larger than expected, and Russia is still delaying and avoiding directly responding to the proposal to deepen OPEC+ production cuts to cope with the sharp drop in demand caused by the coronavirus.

Oil exporting countries The latest monthly report of the Organization of Petroleum Exporting Countries (OPEC) shows that due to the impact of the new coronavirus, it has lowered its forecast for global crude oil demand growth in 2020 by 230,000 barrels/day to 990,000 barrels/day, from the previous value of 1.22 million barrels/day; OPEC crude oil demand forecast is lowered by 200,000 barrels/day to 29.3 million barrels/day; non-OPEC crude oil supply growth forecast in 2020 is lowered by 100,000 barrels/day to 2.25 million barrels/day. In addition, according to secondary data, in January OPEC crude oil production decreased by 509,000 barrels/day to 28.86 million barrels/day; Iran’s crude oil output in January decreased by 9,000 barrels/day to 2.086 million barrels/day; Iraq’s crude oil output in January decreased by 68,000 barrels/day, to 4.501 million barrels per day.

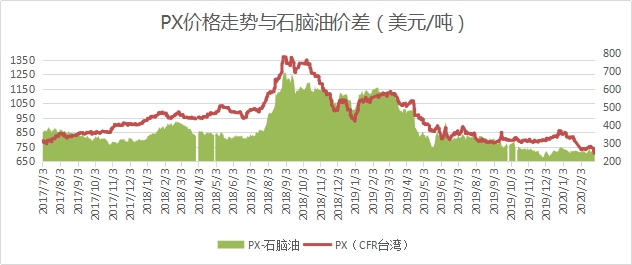

PX price trend

PX prices have fallen sharply by about 6.5% this week following oil prices. On the supply side, some PX factories have shut down for maintenance, but so far, the performance is not obvious. Epidemic The main impact is still on the demand side. The start-up time of polyester companies is mostly postponed to the end of February. The PTA end has high accumulation pressure and the operating rate has dropped significantly. The current PTA operating rate is 79.94%. Considering the production capacity base of 52.39 million tons, the daily output of PTA has decreased. At 14,700 tons, it is equivalent to an annual production loss of 3.5 million tons of PX, accounting for 14.29% of the current total PX production capacity. It is expected that there is great uncertainty in cost-side oil prices, which may drag down PX prices further. Focus on domestic PX installations, crude oil and PTA trends.

Polyester raw materials, PTA weekly trend

Thisweek,thespotpriceofPTAfuturesreturnedtothepathofdeclineduetothesharpdropincost-endcrudeoil.ThedropincrudeoilpriceshascausedthePTAcostlinetomovedownward.AlthoughPTAprocessingfeesareatalowlevel,intheabsenceoffavorablesupportfromsupplyanddemand,itisdifficultforPTApricestodeviatefromrawmaterialprices,andthesupportingroleoflowprocessingfeesistemporarilydifficulttoplay.ThecurrentdomesticPTAinventoryhasclimbedto2.394milliontons,arecordhighforthesameperiodsince2014.Intermsofindustryload,althoughtheaverageloadofdomesticPTAdeviceshasdroppedto79.94%,theloadofpolyesterdevicesisonlyabout60.9%,andtheloadoftheweavingindustryisonlyabout16%.Supplyreductionislimitedanddemandrecoveryisstillinsufficient.Theinventoryofpolyesterproductsisserious,andtheinventoryoffilamentproductsisabout25-37days.Therefore,therecoveryinPTAdemandaftertheholidayisstillnotenoughtoabsorbtheincreaseinsupply.Itisexpectedthatshort-termPTAwillstillmaintainaweakbottomandfluctuate.Itisrecommendedtopayattentiontothemacroeconomicsituation,industrialchaindeviceload,andchangesinterminaldemand.

Polyester raw material, MEG Weekly trend

Ethylene glycol performed slightly stronger this week, only falling slightly by about 1.66%. The start-up load of polyester companies has declined, causing the consumption of ethylene glycol to also perform poorly. As of February 21, the domestic port inventory of ethylene glycol in East China was 538,000 tons, an increase of 234,000 tons from the low in late December 2019, an increase of 76.97%. In this case, ethylene glycol production companies were forced to reduce their loads and limit production to protect prices. As of February 21, the domestic ethylene glycol operating load was only 68.95%, down 10.47% from the same period last year. At present, although the overall consumption of the chemical fiber industry is sluggish due to the impact of the epidemic, which has greatly suppressed the price of ethylene glycol, the inventory pressure of domestic ethylene glycol is actually far lower than the level of one million tons in the same period last year. . It is expected that ethylene glycol will mainly fluctuate in the short term. Focus on industrial operation and commodity atmosphere.

</p